FAQ Audits and Accounts

Q. What are Central Autonomous Organisation ?

Ans: There are nearly 500 central autonomous organizations in the country. Most of them are registered under the Societies Registration Act, 1860. Some of them have been created under specific Acts of Legislature. They have no owners, unlike Companies, Partnership or Proprietary concerns. However, all of them have been created by the nodal Ministries in the Government of India as promoters. Each one of them has a Memorandum of Association defining their objects and Rules, Regulations and Byelaws governing the operations, organizational structure, (General Body, Governing Body and the Executive head of the organization). Powers of the General Body Governing Body (Council) and the Executive head, Finance and Accounts, Time limits for preparation of Annual financial statements and their placement before the Governing body or General Body for approval, Meetings of Governing Body (Council), General Body for approval, Meetings of Governing Body (Council), General Body, etc., Audit, Parliament’s Control, etc. These are comparable to the Memorandum of Association and Articles of Association and Articles of Association of Companies.

Q. What are financial resources?

Ans: Almost all the autonomous organizations are dependent on grants from the Govt. of India to meet their capital expenditure requirements. Many of their activities are included in the Five Year Plans of the Nodal Ministries of Govt. of India. Some of them are dependent on the Govt. of India (and State Governments) for non-plan grants to meet their deficit on Revenue Account. These are substantial particularly in the case of research organizations such as ICAR, CSIR, ICMR, etc., and Central Universities and Institute of Higher education

Q. Who Audits the Accounts?

The accounts of most of the autonomous organizations particularly those created under specific Acts of Legislature are audited by the Comptroller and Auditor General of India as the sole auditor. The accounts of some of them are audited by firms of Chartered Accountants. As they also enjoy grants from Government of India, they are in addition subjected to Grant-in-Aid audit by the Comptroller and Auditor General of India.

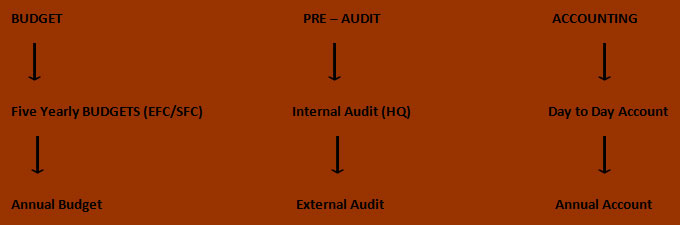

Q. What is the Function of finance & accounts section?

Ans:

Q. What is the System of PROJECT ACCOUNTING?

Ans:

- Accounting Centers – Project implementation unit.

- Separate bank accounts for the project

- Accrual accounting system that is the double entry system of accounting to be followed

- Quarterly SOE to be submitted

- Final accounts (Balance Sheet, Income -Expenditure and Receipt and Payment) to be prepared.

Q. What are the Records to be maintained Pertaining to Project?

Ans:

- Cash Book (Main & Subsidiary)

- Cheque Book /Demand Draft Register

- Valuable Register

- Project wise & Head wise Expenditure Register.

- Budget Control Register

- Asset Register & Liability Register

- Advance Register

- Objection Book etc.

- Contractor’s Book etc.

- Contractor’s Ledger

- Supporting documents for SOE to be kept for post review by the Funding Agency.

- All the documents relating to project expenditure to be kept for 5 years after the completion of the project.

Q. Auditing of the project?

Ans:

- Internal Audit

- External Audit

With the objective that individual expenditure included in the SOE is fully supported by documentation.

Expenditures are properly authorized by the authorized persons & is in accordance with the rule.

The expenditure are properly accounted for

Internal Audit

INTERNAL Audit done on regular basis by the finance & accounts Officer of the Institute. The Internal Audit will also be carried out by the internal audit team from the finance section if need be. The internal audit will be decided on the basis of magnitude of expenditure and risk perceived.

External Audit

External Audit for ICAR/CSIR other similar institutes and Government departments will be done by C&AG. For SAUs the audit will be conduct by state AGs/Local fund auditor/C.A.

Q. What is Financial governance ?

Ans:

- Inspection at periodic intervals by Funding Agency to monitor financial management

- Funds to be utilized of bonafide/intended purpose using norms and procedure

- Expenditure to be kept within the approved allocation

- All basic records to be maintained

- All advances to be adjusted within the prescribed time limit but before close of the financial year

- All procurements will be made following GFR Guidelines

Q. What is Assessment/ Quantifying?

Ans: Assessed/quantified by following means:

- Increase in productivity – Either in case of agriculture/animal science, the increase in productivity through intervention made with the help of the project implementation could be quantified in terms of currency. (Money Value)

- 2. Ecosystem Services- The services, in the form of binding the soil and maintaining its organic and inorganic properties, regulating hydrological cycles that drinking water, conversion of carbon dioxide into oxygen through photosynthesis, and shelter to a fauna is unparalleled and not easily quantifiable in economic terms. Many indirect benefits which we get through implementation of the project cannot be quantified in terms of monetary gains. However, it is a act that many of the projects, particularly related to agroforestry etc. could provide many ecosystem services.

- Socio- economic aspect – It’s a long term monitor able target in terms of finance since the interventions could make the impact in terms of increase in productivity and therefore, profitability.

Q. What is OUTPUT/OUTCOME?

- It differs with the kind of research being done, viz. in case of extension research, the outcome could be assessed in terms of in situ moisture conservation, increase in cropping intensity and thereby net gain in round the year need based employment to the farming family, conservation of natural resources and ultimately net increase in productivity. In case of strategic research, the outcome could be assessed by adoption rate of the interventions made in any field of agriculture, whereas the outcome of fundamental research could be assessed as to how it has helped in developing the strategic/extension projects. This research acts as a pillar stone and provides strength for the cause of crop productivity, profitability etc.